Unemployment a Lagging Indicator?

Charles Plosser, president of the Philadelphia Federal Reserve, coming from the Fed meeting, told CNBC in an interview that he sees some clear positives about the economy. CNBC, in their endless campaign to report only good financial news and to cheerlead falsified economic reports was right there with him. He completely dismissed unemployment and called it a lagging indicator of economic recovery.

Charles Plosser, president of the Philadelphia Federal Reserve, coming from the Fed meeting, told CNBC in an interview that he sees some clear positives about the economy. CNBC, in their endless campaign to report only good financial news and to cheerlead falsified economic reports was right there with him. He completely dismissed unemployment and called it a lagging indicator of economic recovery.

I don’t know about you, but any practical economist knows that when demand picks up the very first thing you do is not order double your current inventory, but you instead opening up hiring in anticipation of the demand. You know your inventory is low, and you also know you’re understaffed. Efficiency, always tells you that being understaffed is just as economically dangerous as being low in supplies, if not worse. If you’re low on inventory, you can raise prices and recoup on the perceived lost value, but you can’t raise prices to account for understaffing.

Commericial Real Estate

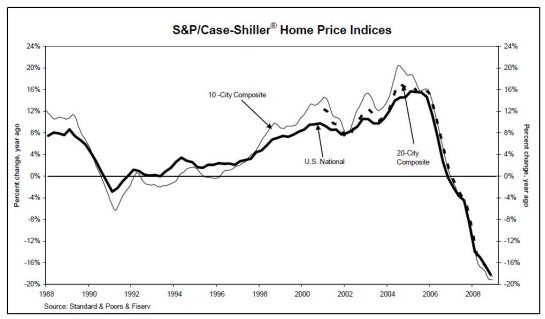

He also dismissed commercial real estate defaults and said it was a “concern” only insofar as it relates to financial institutions. He said that there was stabilization in the housing market. Which is a complete lie.

- There are over $1 trillion in housing inventory which has not been put on the market.

- Banks stopped putting this inventory on the market to shore up cliff diving housing prices.

- The Federal Reserve lowered interest rates to stop the plummet of housing prices.

- Obama passed a stimulus bill which included a cash incentive to buy a house sort of like the cash for clunkers program.

What he is also leaving out is that ARM loans and Alt-A loan defaults have yet to hit the market, to the tune of $2 trillion. Along with this the commercial real estate defaults are said to hit the market to the tune of $1 trillion. There is no stabilization in housing prices. Housing prices have been halted by infusing trillions of dollars into the market. When that money is removed, housing prices will once again resume plummeting. They should be back down to 1980’s market prices, according to experts.

Exit Strategy of the Fed and Raising Interest Rates

Plosser completely dismissed the notion that the Fed would raise interest rates this year. He also dismissed inflation as plausible for over 2 years. He clearly lives in a glass bubble that has absolutely no balance sheets on the price increases for the past 2 years, since the first bailouts started hitting.

The Federal Reserve balance sheet has shot up since last year from $750B to a staggering $2.25T. It owns $5T in government securities on top of its current balance sheet. That is to say, the U.S. government owes yearly $8 trillion to the Federal Reserve. Every single tax dollar that it collects from commerce, imports, and personal incomes goes to just pay off the interest owed on that $8 trillion. To fund all of the welfare, medicare, medicaid, farm subsidies then, the government has to turn around and borrow more money from the Federal Reserve.

He did not admit that the Federal Reserve has consistently overstepped the bounds of actually making fiscal policy without any input or approval of congress. He did not admit that small and medium businesses, the largest employers in this economy, ever received any stimulus or credit or flow of capital that was said to have gotten to them to get the recovery going.

Plosser did say he did not expect a V shaped recovery, nor a W, but an actual L shaped recovery, meaning that he did not expect us to ever reach the former perceived levels. This is simply hedging his bets so that the Federal Reserve is off the hook come time for the real recovery to start happening and the Fed withdrawing the stimulus money and loans.

Please visit my legal website: Las Vegas DUI Attorney

See me on YouTube: Shakaama Live